Formalizing the Code

Presenter: Michael

Preview

Michael will present “Formalizing the Code” by Sarah Lawsky.

Internal Revenue Code

The Internal Revenue Code (IRC) is complex because of dependencies (interlinked sections of the Code)

- Cross-references explicitly call other definitions

No gain or loss shall be recognized if property is transferred to a corporation by one or more persons solely in exchange for stock in such corporation and immediately after the exchange such person or persons are in control (as defined in section 368(c)) of the corporation.

- Definitions implicitly call earlier language

This paragraph shall not apply to any redemption made pursuant to a plan the purpose or effect of which is a series of redemptions resulting in a distribution which (in the aggregate) is not substantially disproportionate with respect to the shareholder.

Definitional Scope Problem

- Definition

A set of words that can be substituted throughout the text for another word or set of words, salva veritate 1

- Problem

Code uses a term, but the structure 2 of the Code leaves unclear to what a term refers

- Example

Main Rule: If A is X, then B.

Definition: X means [definition].

Limitation: This section applies only if A has characteristic Y.

Other Rule: If A is X, then C. What if A is X, but A does not have characteristic Y? Does C hold?

- Unintentional Ambiguity

Spend time and money determining meaning or litigation

Reduce voluntary compliance

Ambiguous provisions leads to increased audits

You may notice a similarity to the lexical vs dynamic scoping problem

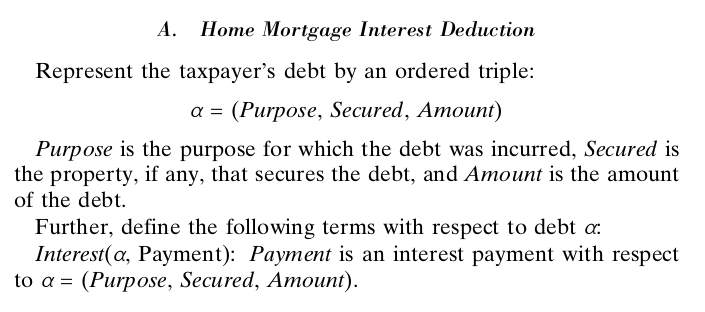

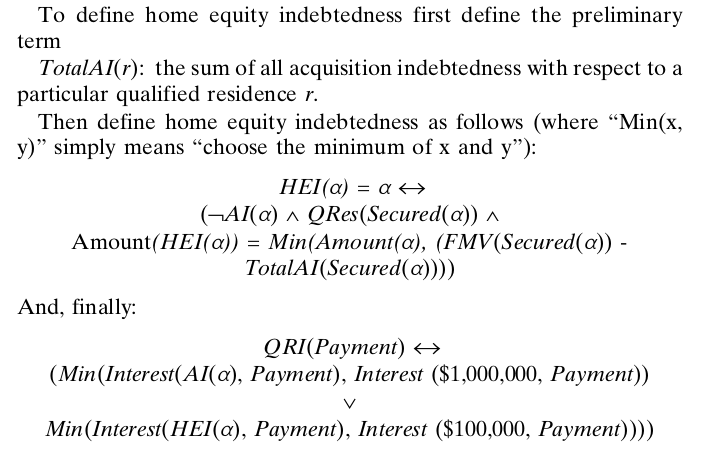

Example 1: Home Mortgage Interest Deduction, $\S$ 163(h)

- Deductible Interest Payments

Non-personal interest payments are deductible 3

- Personal Interest Payments

All except six discrete items, which include “qualified residence interest”

- Qualified Residence Interest

- Acquisition Indebtedness (AI)

Debt incurred in acquiring, constructing, or substantially improving any qualified residence of the taxpayer, and is secured by such residence

- Home Equity Indebtedness (HEI)

Debt that is not AI that is secured by the qualified residence and

It doesn’t exceed fair market value of residence reduced by AI

Total amount treated as HE cannot exceed $100,000

- Example

Seymour purchases $1.4 million residence

$300,000 cash

$1.1 million purchase money mortgage

$88,000 interest per year

First $1 million is deductible w.r.t. AI, so only $80,000 is deductible

Remaining $100,000 is HEI

- Remaining $8,000 interest is deductible

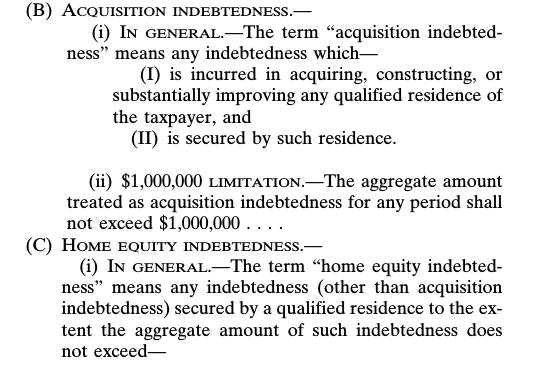

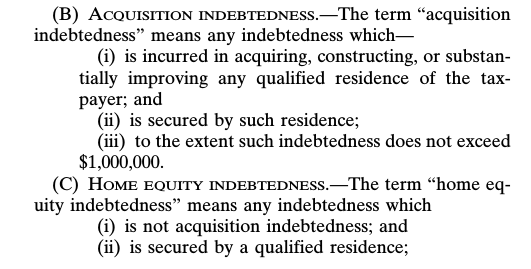

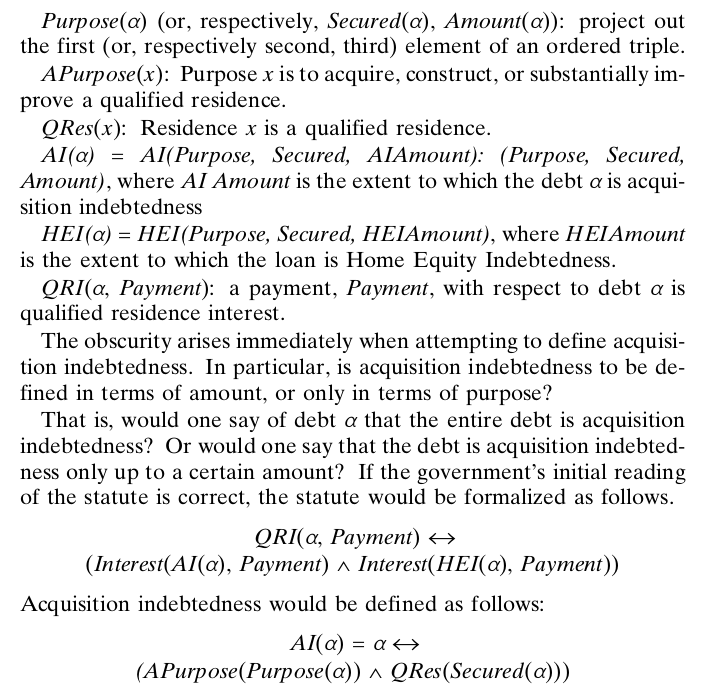

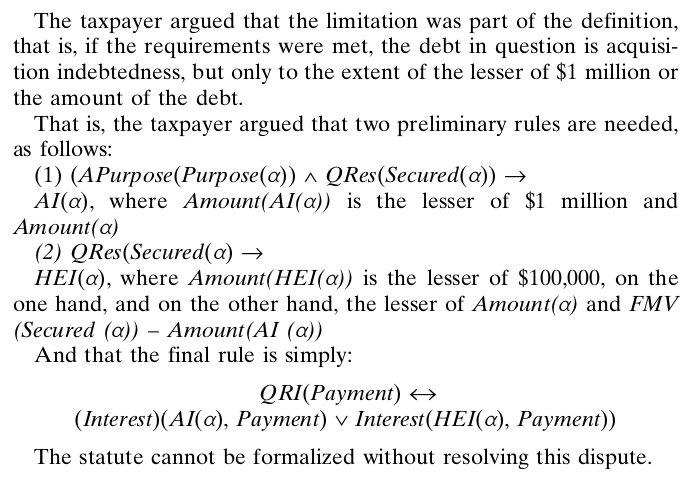

- Problem

$\S$ 163(h) uses term “acquisition indebtedness” in definition of HEI

Is AI on total indebtedness, or only up to $1 million under limitation provision?

If former, than the $100,000 past $1 million is not HEI

Tax court

First ruled former, that petitioner did not demonstrate $100,000 was no used in acquiring house

Then ruled latter, that $1 million limitation was part of definition of acquisition indebtedness, so indebtedness in excess was not AI

Before Fix

After Fix

Example 2: Substantially Disproportionate Corporate Distribution

- Corporate Redemption

Corporation acquires its own stock from shareholder in exchange for money or other property

Can be treated as a sale of stock or a distribution (and possibly a tax-deductible dividend), depending on \(\S\) 302

If redemption not captured by one of five situtions, including \(\S\)302(b)(2), it is a distribution

- Substantially Disproportionate \(\S\)302(b)(2)

Shareholder’s percentage ownership of voting stock after redepemtion < 80% of prior ownership

Same (< 80%) with respect to common stock

- Example

Corporation has 100 shares of voting stock

Shareholder A owns 80% (80/100)

Corporation redeems 50 shares of A

A now owns 60% (30/50)

Two 80% tests pass

- 60% < 80% * 80% = 64%

Redemption is substantially disproportionate, so a sale

Limitation in \(\S\)302(b)(2)

- Not SD if > %50

- Problem

Another provision uses SD definition, but ambiguous on whether the 50% limitation is included in that definition

Legislative history, claimed as purpose by court, is incorrect in its exposition

Resolution

- Incorporate limitations meant to be included in definitions into respective “definitions” sections

Formal Logic

Use first-order logic (see also: default logic)

Benefits

Drafters formalize proposed language to check structure of language (rather than including formalization in statute itself)

Identify (not automatically resolve) ambiguity

Encourage symbolic formalization of legislation for legibility by a computer

- Reason about law, not simply translate tax forms like TurboTax

Lower litigation and compliance costs

Ambiguities

- Most unintentional

Formalization Example

Relevant Other Sources

[1] L. E. Allen, “Symbolic Logic: A Razor-Edged Tool for Drafting and Interpreting Legal Documents,” The Yale Law Journal, vol. 66, no. 6, p. 833, May 1957.

[2] A. Scalia, G. O. R. D. O. N. S. WOOD, L. A. U. R. E. N. C. E. H. TRIBE, M. A. R. Y. A. N. N. GLENDON, and R. O. N. A. L. D. DWORKIN, A Matter of Interpretation: Federal Courts and the Law, STU - Student edition. Princeton University Press, 1997.

[3] S. Breyer, “On the Uses of Legislative History in Interpreting Statutes The 1991 Justice Lester W. Roth Lecture,” Southern California Law Review, vol. 65, pp. 845–874, 1991.

[4] K. D. Ashley, “Teaching Law and Digital Age Legal Practice with an AI and Law Seminar,” p. 63, Jun. 2013.

[5] T. Bench-Capon et al., “A History of AI and Law in 50 Papers: 25 Years of the International Conference on AI and Law,” Artificial Intelligence and Law, vol. 20, no. 3, pp. 215–319, Sep. 2012.

[6] L. T. McCarty, “Reflections on ‘Taxman’: An Experiment in Artificial Intelligence and Legal Reasoning,” Harvard Law Review, vol. 90, no. 5, p. 837, Mar. 1977.

[7] L. K. Branting, “Data-Centric and Logic-Based Models for Automated Legal Problem Solving,” Artificial Intelligence and Law, vol. 25, no. 1, pp. 5–27, Mar. 2017.